Latest NatWest South East Growth Tracker data reveals renewed activity growth, fuelled by greater new order inflows and amid a notable improvement in confidence.

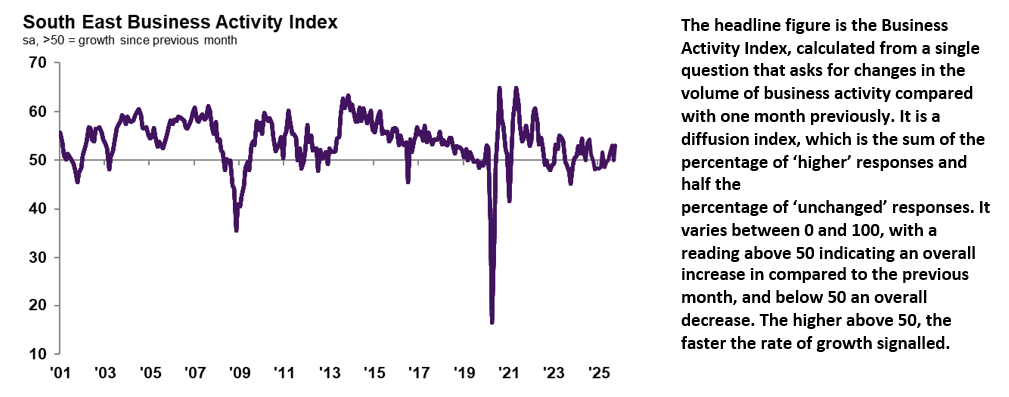

Up from September’s neutral 50.0 reading, the headline South East Business Activity Index posted at 53.1 in October. This was consistent with a moderate increase in output that was back in line with that seen in August.

With that, the rate of growth was the joint-fastest in 14 months. The expansion in output was often linked by panellists to higher new business volumes.

October survey data signalled a third successive monthly rise in the volume of new orders placed with firms across the South East.

In anecdotal evidence, companies commented on signs of improvement in demand conditions as well as the securing of new contracts. The rate of expansion was not only marked but also the strongest recorded since May 2023.

Looking ahead, firms based in the South East expressed a stronger degree of confidence that output levels would rise over the coming 12 months. Growth strategies, strong new business pipelines and investment in advertising, marketing and machinery were reasons supporting firms’ upbeat forecasts.

The level of confidence improved so much that it was back above its long-run average and the most upbeat in just over a year.

Catherine van Weenen, territory head of Commercial Mid Market at NatWest, said: “After having stalled in September, the South East economy entered the final quarter on a more stable footing and with business activity back inside growth territory.

“Notably, the South East placed second in the regional rankings, behind London, with respect to output, new orders and business expectations.

“The improvement in demand conditions was starting to be felt in labour market outcomes, as the rate of job losses was the weakest in over a year and firms’ ability to clear backlogs was not as strong as in recent months.

“There was also some good news on the price front, as input cost inflation retreated to its lowest in nearly a year, which allowed companies to raise their charges at a softer rate.”

Of the 12 monitored UK regions and nations, the South East was one of six UK areas to see a rise in output in October. Only London recorded a faster rate of activity growth than that seen locally.

Likewise, the South East signalled the second-fastest rise in new work, behind only London. In line with this, on average, only firms in London were more confident that those in the South East.

The seasonally adjusted Employment Index remained below the neutral 50.0 mark in October, signalling a 14th consecutive monthly reduction in headcounts across the South East economy.

The rate of reduction was only marginal, however, and the least marked seen over this period. It was also just softer than the UK-wide trend.

While on one hand companies linked lower payroll numbers to the non-replacement of leavers, due to elevated wage costs and uncertainty, the decline was cushioned by increased hiring at some firms in line with new business growth.

Although there were existing signs of spare capacity, as signalled by another decrease in backlogs, the rate of depletion was the least marked in six months. Firms noted having sufficient capacity to work through outstanding orders.

The South East’s trend of depletion in orders outstanding was broadly in line with that seen at the national level.

Operating expenses faced by firms in the South East increased again at the start of the final quarter of 2025. Companies widely reported that the cost of wages, raw materials and utilities had gone up, as well as service fees.

Although still substantial and elevated by historical standards, the rate of cost inflation eased to its lowest in nearly a year. Cost pressures in the South East were just softer than on average across the UK.

As has been the case on a consistent basis for just over five years, October data indicated an increase in average prices charged for the provision of South East goods and services. The rate of inflation was the least marked since July, but still strong overall and elevated compared to the UK-wide trend.

While firms principally increased charges due to higher costs, there were some instances of discounting due to price competition.